Oravel Stays Limited

Fundamentals

| ORAVEL STAYS LIMITED (Oyo) Unlisted Shares Price | Rs 26.5018 Per Equity Share | Market Cap (in cr.) | Rs 37137 |

| Lot Size | 1000 Shares | P/E Ratio | 155.89 |

| 52 Week High | Rs 56 | P/B Ratio | 9.82 |

| 52 Week Low | Rs 26.5018 | Debt to Equit | 1.89 |

| Depository | NSDL & CDSL | ROE (%) | 6.47 |

| PAN Number | AABCO6063D | Book Value | 2.7 |

| ISIN Number | INE561T01021 | Face Value | 1 |

| CIN | U63090GJ2012PLC107088 | Total Shares | 140131105220 |

| RTA | Link Intime |

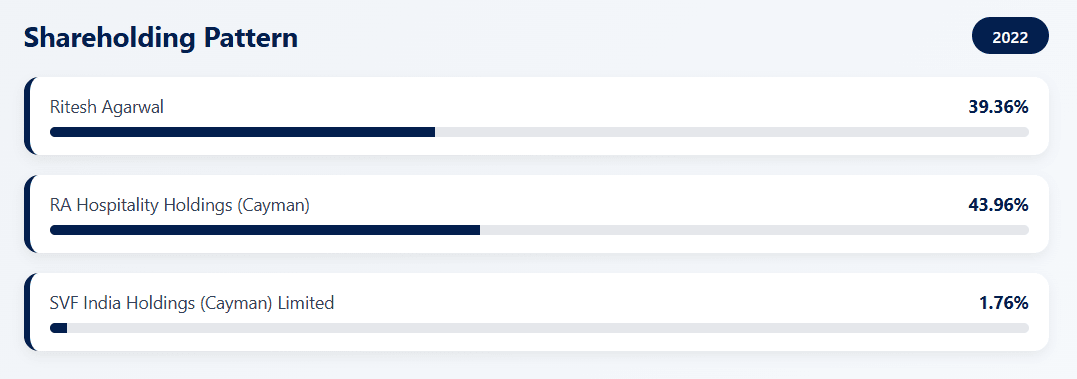

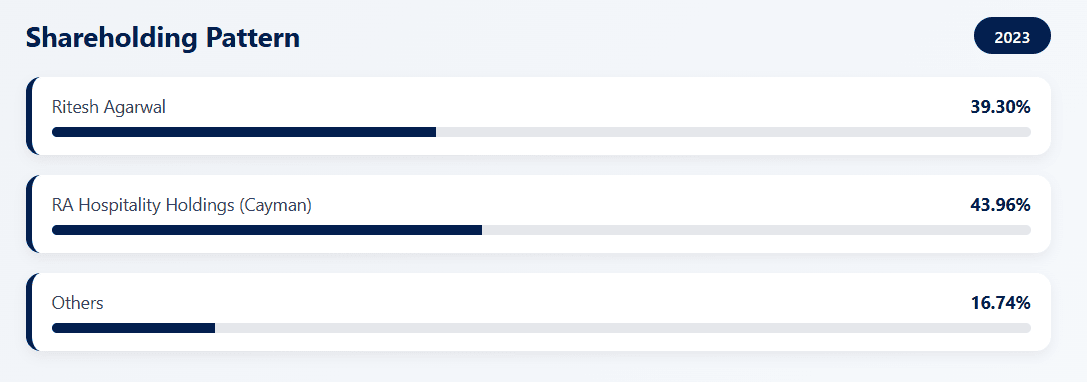

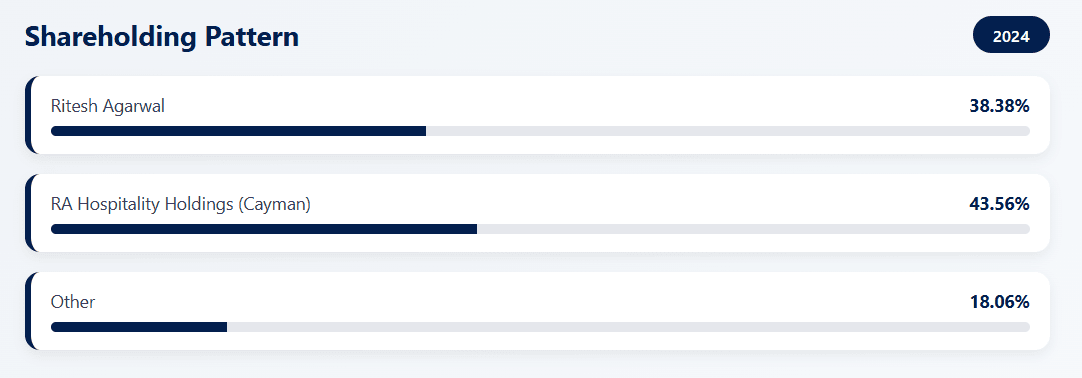

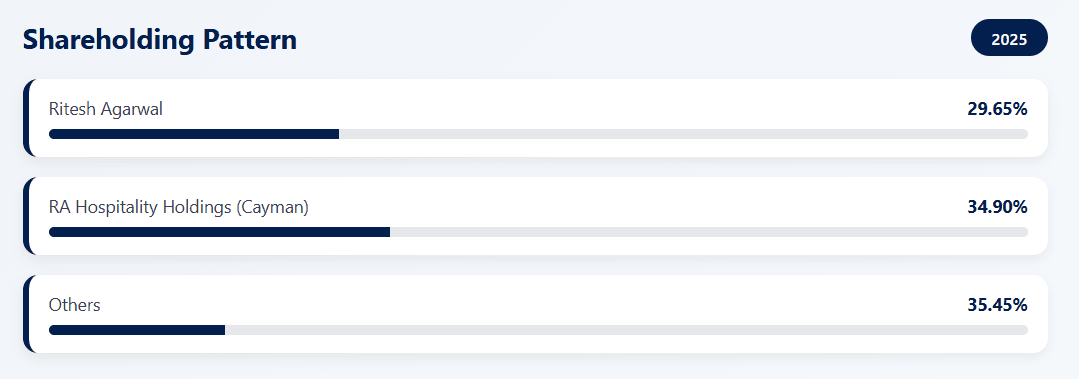

Shareholding Pattern

Oravel Stays Limited (OYO)

Founded by Ritesh Agarwal, Oravel Stays is the parent company of the global hospitality brand OYO. In 2025, it rebranded as PRISM to represent its growth into a diversified holding company managing international assets like Motel 6 and Studio 6. Operating across 35+ countries, the group leverages a proprietary tech platform to standardize budget and midscale accommodations.

As a private entity, PRISM oversees corporate strategy, fundraising, and governance for its vast ecosystem of hotels and vacation rentals. The transition to the PRISM brand signals a shift from a single-brand startup to a multi-brand global hospitality leader. Currently, the company focuses on improving profitability as it prepares for a potential IPO of the OYO business.

Company Business Model

Oravel Stays Limited operates an asset-light hospitality platform model, aggregating and franchising hotels, homes, and alternative accommodations under the OYO brand.

Hotel Aggregation & Franchising

Partners with property owners to standardize rooms under the OYO brand in return for revenue share / franchise fees.

Technology Platform

Uses pricing algorithms, demand forecasting, and booking technology to optimize occupancy and room yields.

Online Distribution

Generates bookings through its app, website, and OTA partnerships, earning commissions and platform fees.

Ancillary Services

Monetizes value-added services such as branding, marketing, operations support, and financing assistance to hotel partners.

Competitors

Oravel Stays (OYO) competes in the asset-light hospitality, hotel aggregation, and online accommodation space with the following players:

Treebo Hotels

Budget hotel chain using a franchise and managed-hotel model.

FabHotels

Aggregates and operates budget hotels focused on metro cities.

MakeMyTrip

OTA offering hotels, homestays, and alternative accommodations.

Goibibo

Strong hotel booking platform competing for the same inventory.