Hero FinCorp Limited

Fundamentals

| Hero Fincorp Limited Unlisted Shares Price | Rs 1175 Per Equity Share | Market Cap (in cr.) | Rs 14969.5 |

| Lot Size | 25 Shares | P/E Ratio | 136.15 |

| 52 Week High | Rs 1925 | P/B Ratio | 2.59 |

| 52 Week Low | Rs 1150 | Debt to Equit | 8.33 |

| Depository | NSDL & CDSL | ROE (%) | 1.91 |

| PAN Number | AAACH0157J | Book Value | 452.86 |

| ISIN Number | INE957N01016 | Face Value | 10 |

| CIN | U74899DL1991PLC046774 | Total Shares | 127400000 |

| RTA | Link Intime |

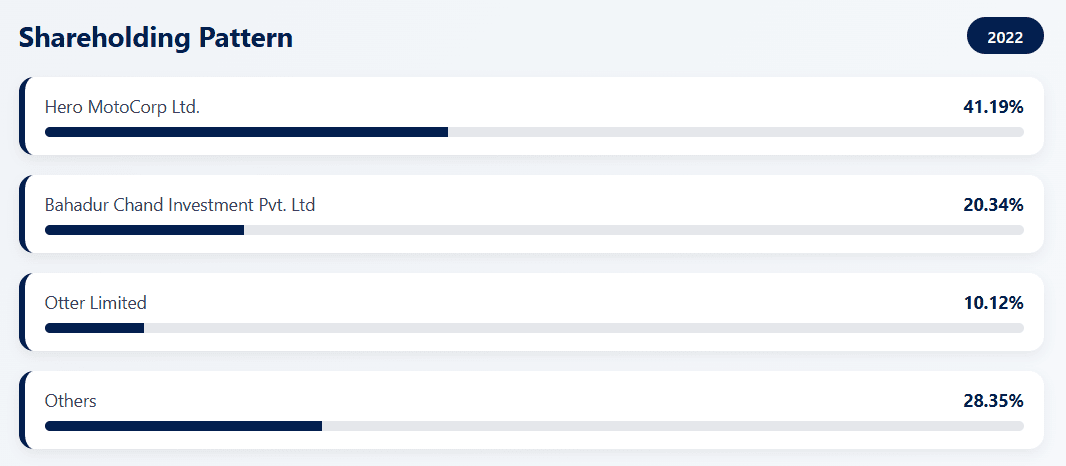

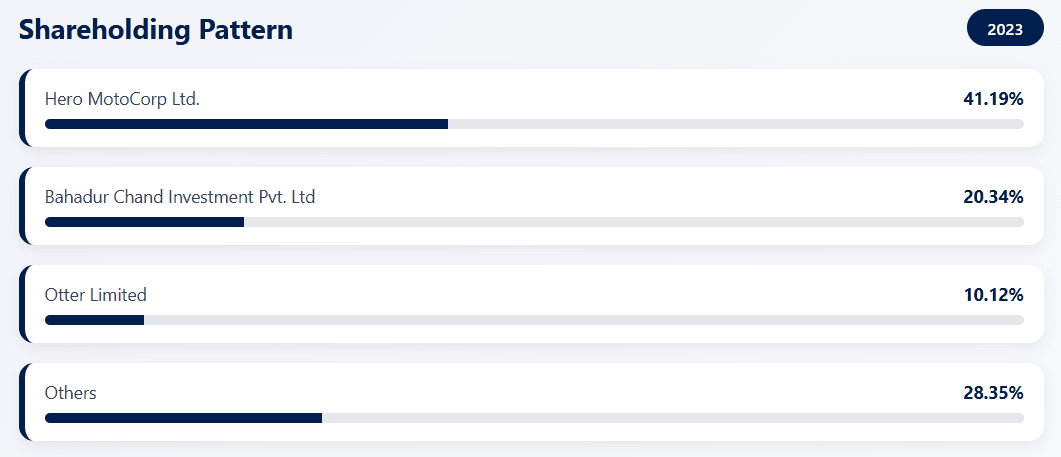

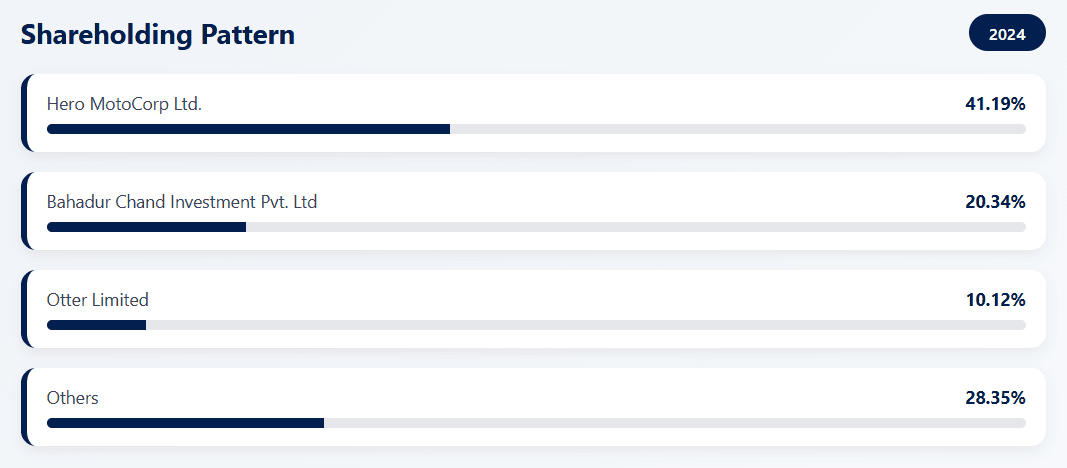

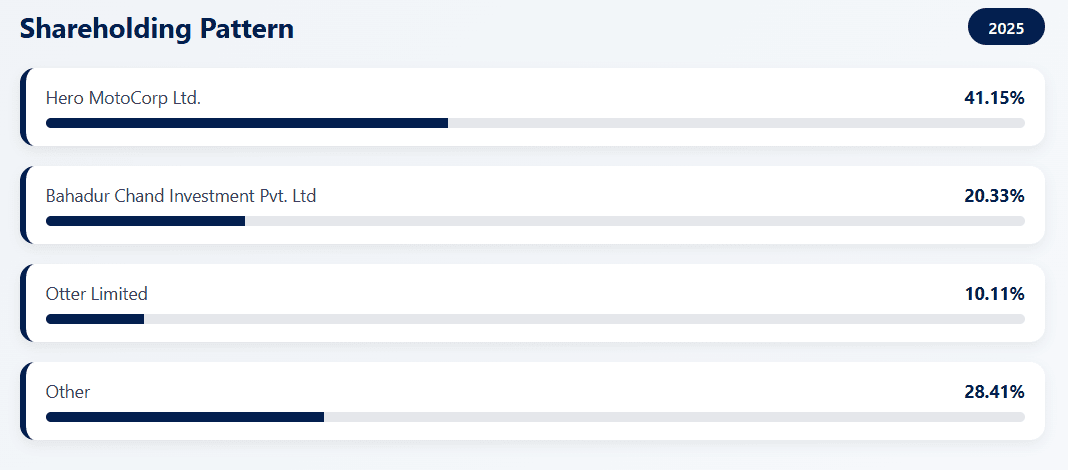

Shareholding Pattern

Hero FinCorp Limited

Founded in 1991, Hero FinCorp is a prominent Indian NBFC within the Hero Group, led by MD & CEO Abhimanyu Munjal. Originally a captive financier for Hero MotoCorp, it has evolved into a diversified lender providing retail, SME, and corporate financing across India. Its product suite includes vehicle and personal loans, alongside working capital and bill discounting for MSMEs.

By leveraging an extensive dealership network and advanced data analytics, the firm significantly boosts credit access in both urban and rural markets. Supported by global equity investments, Hero FinCorp is currently focused on digital transformation and financial inclusion. It remains a key player in India's fast-growing financial services sector, driven by the rising demand for retail and small business credit.

Company Business Model

Hero FinCorp Limited operates a non-banking financial company (NBFC) lending model, focused on retail, MSME, and corporate credit in India.

Retail Lending

Provides personal loans, two-wheeler loans, and consumer finance products to individuals, leveraging the Hero Group's distribution reach.

MSME & Corporate Lending

Offers working capital loans, business loans, and structured finance to small businesses and corporates.

Risk & Credit Underwriting

Uses data-driven credit assessment and risk management to control NPAs and optimize returns.

Interest-Based Revenue Model

Generates income primarily through interest on loans, along with processing fees and ancillary charges.

Competitors

Hero FinCorp operates in India's NBFC lending space and competes with the following players:

Bajaj Finance Limited

Market leader in consumer finance and personal loans with strong digital capabilities.

Tata Capital Limited

Diversified NBFC offering retail, MSME, and corporate lending.

HDFC Ltd

Strong competitor in retail and secured lending (now merged into HDFC Bank).

L&T Finance Limited

Focused on rural, MSME, and infrastructure-linked lending.