Care Health Insurance Limited

Fundamentals

| Care HealthLimited Unlisted Shares Price | Rs 138 Per Equity Share | Market Cap (in cr.) | Rs 13,444 |

| Lot Size | 500 Shares | P/E Ratio | 86.79 |

| 52 Week High | Rs 186 | P/B Ratio | 5.67 |

| 52 Week Low | Rs 138 | Debt to Equit | N/A |

| Depository | NSDL & CDSL | ROE (%) | 6.53 |

| PAN Number | AADCR6281N | Book Value | 24.36 |

| ISIN Number | INE119J01011 | Face Value | 10 |

| CIN | U66000DL2007PLC161503 | Total Shares | 97,418,460 |

| RTA | KFin Technology |

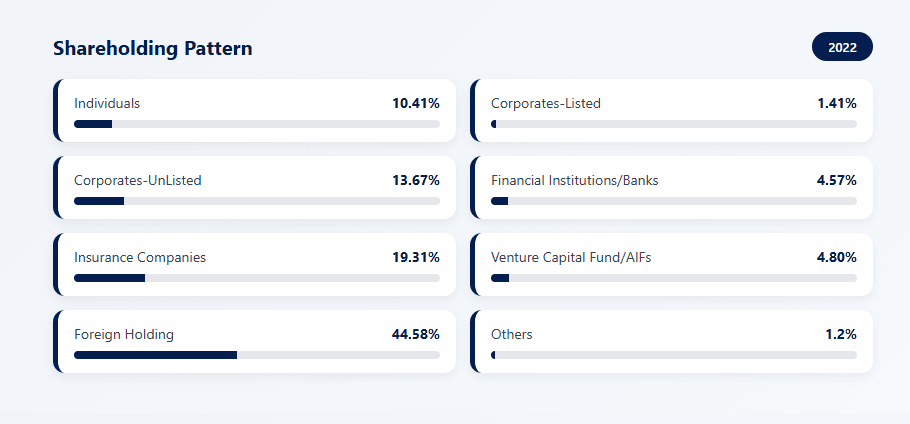

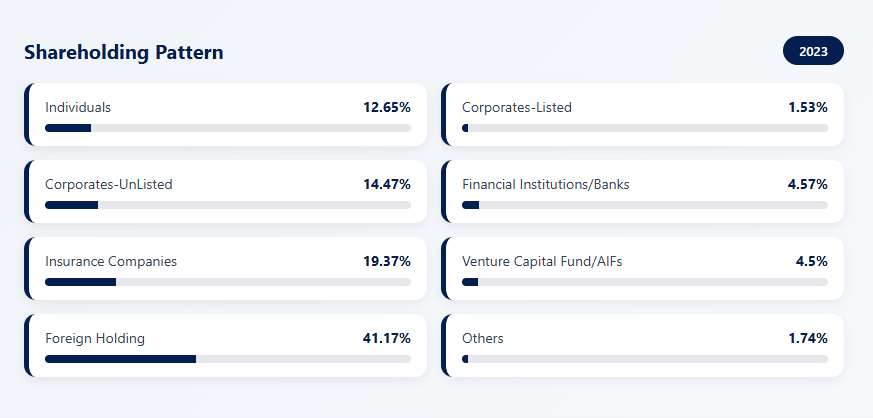

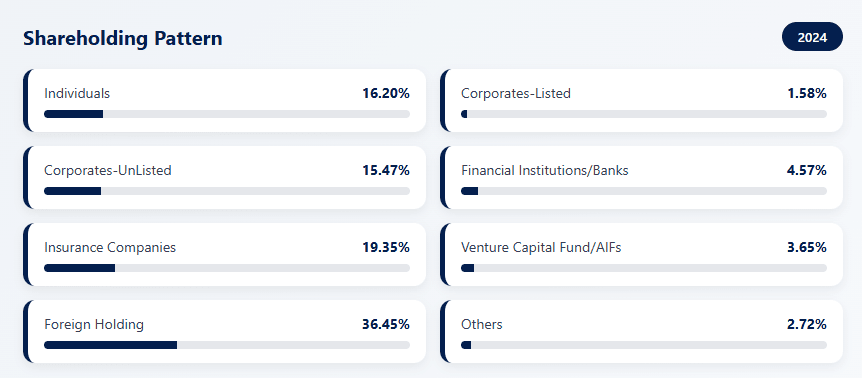

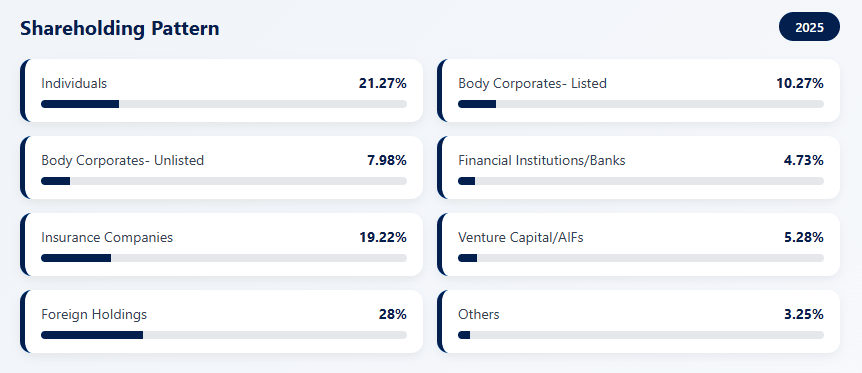

Shareholding Pattern

Care Health Insurance Limited

Care Health Insurance, formerly Religare, is a major Indian standalone health insurer based in Gurugram. As a subsidiary of Religare Enterprises, it provides retail, group, and travel insurance nationwide. Its portfolio includes specialized covers for critical illnesses, maternity, and high-value "Care Supreme" plans. The company operates a digital-first model, using a mobile app for policy management and claims. With over 24,800 cashless hospital partners, it ensures broad healthcare access for all policyholders. In 2025, it was awarded "Best Claim Settlement Company" for its high efficiency and service. The firm distributes products through a mix of agents, bank partners, and online digital aggregators. It remains a top market competitor by offering innovative features like automatic sum insured recharge.

Company Business Model

Care Health Insurance Limited operates a standalone health insurance business model, focused exclusively on underwriting and servicing health-related insurance products in India.

Retail Health Insurance

Generates premium income from individual and family health policies, including mediclaim and critical illness covers.

Group & Corporate Insurance

Provides health coverage to employers, corporates, and institutions through group health policies.

Claims Management

Earns through efficient claims processing and cost control via hospital networks and TPAs.

Distribution-Led Growth

Sells policies through agents, brokers, bancassurance partners, and digital channels.

Competitors

Care Health Insurance operates in India's health insurance space and competes with the following players:

Star Health and Allied Insurance

The largest standalone health insurer, dominating retail mediclaim and senior citizen health policies with a wide hospital network.

Niva Bupa Health Insurance Company

Competes strongly in retail and corporate health insurance, backed by global healthcare expertise from Bupa.

ManipalCigna Health Insurance

Focuses on health and wellness-led insurance products, leveraging Manipal's healthcare ecosystem.

HDFC ERGO General Insurance

A strong indirect competitor offering comprehensive health insurance along with other general insurance products.