Apollo Green Energy Limited

Fundamentals

| Apollo Green Energy Limited Unlisted Shares Price | Rs 84 Per Equity Share | Market Cap (in cr.) | Rs 314 |

| Lot Size | 500 Shares | P/E Ratio | 10.04 |

| 52 Week High | Rs 335 | P/B Ratio | 0.51 |

| 52 Week Low | Rs 78 | Debt to Equit | 0.74 |

| Depository | NSDL & CDSL | ROE (%) | 5.11 |

| PAN Number | AAACA6447N | Book Value | 166.22 |

| ISIN Number | INE838A01015 | Face Value | 10 |

| CIN | U74899DL1994PLC061080 | Total Shares | 40610287 |

| RTA | Alankit Assignments |

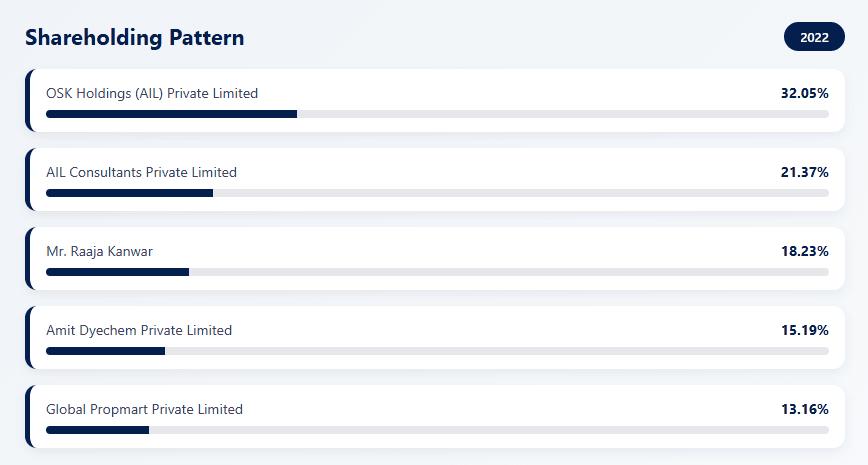

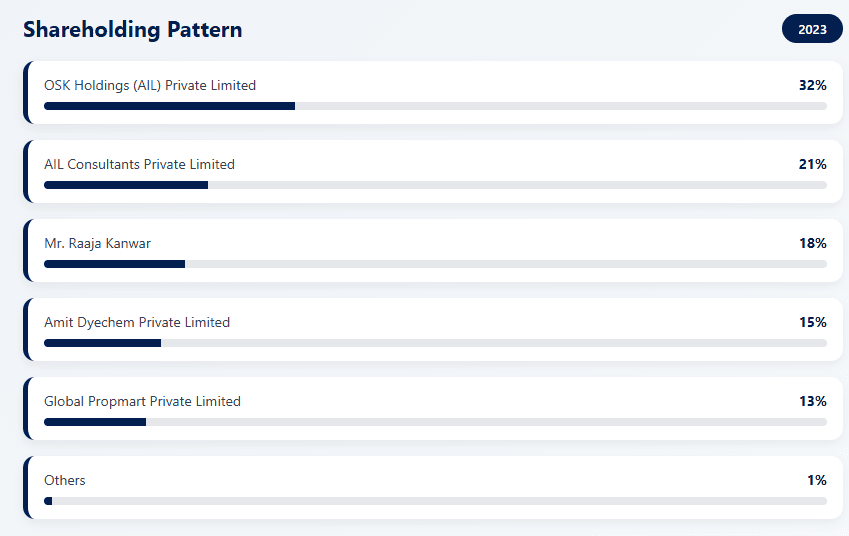

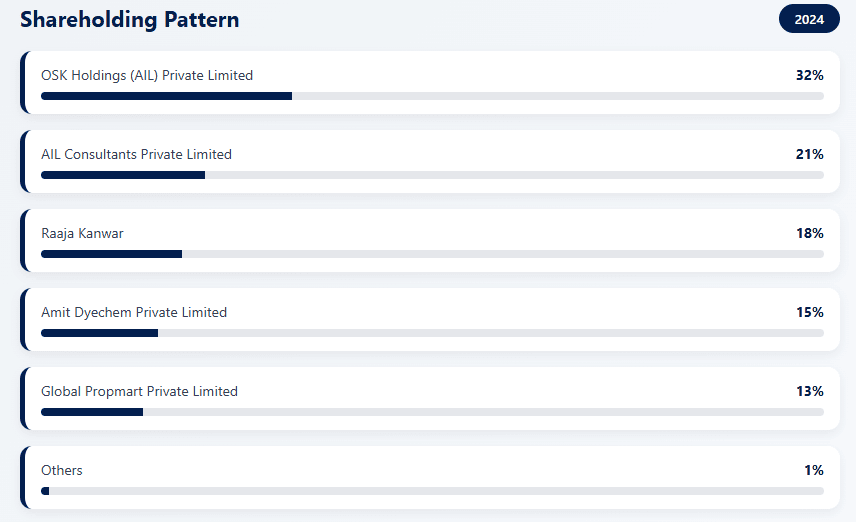

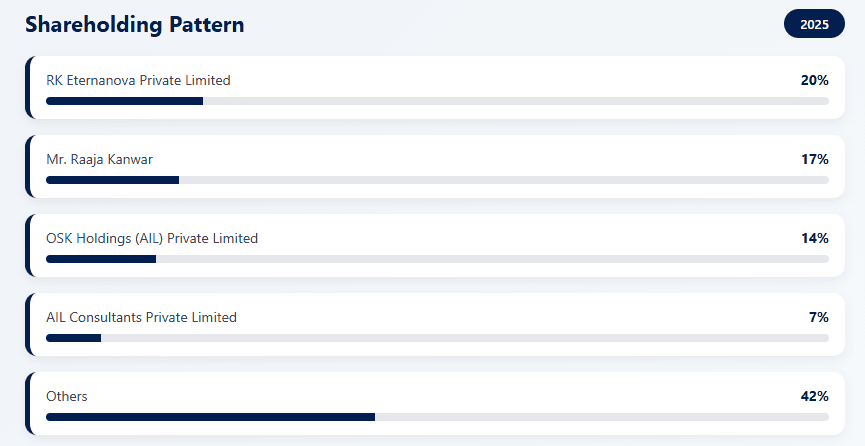

Shareholding Pattern

Apollo Green Energy Limited

Apollo Green Energy Limited (AGEL), a subsidiary of the Apollo International Group, is a prominent Indian EPC firm specializing in utility-scale solar, wind, and hybrid energy solutions. Currently managing an order book of approximately Rs 3,500 crore, the company aims to scale its portfolio to Rs 10,000 crore by 2026 while expanding into green hydrogen and battery storage. AGEL is also vertically integrating its operations through a 500 MW solar module manufacturing plant in Madhya Pradesh and a major Rs 4,500 crore solar investment in Odisha. With a reported net profit of Rs 44.36 crore in FY25, the firm is strategically preparing for an IPO in 2026 to transition from a construction-focused provider to a large-scale independent power producer.

Company Business Model

Apollo Green Energy Limited operates a renewable energy EPC (Engineering, Procurement & Construction) business model, focused primarily on utility-scale solar power projects.

EPC Services

Designs, engineers, procures, and constructs large solar power plants for government bodies, PSUs, and private developers.

Turnkey Solutions

Delivers end-to-end execution including land development, civil works, module installation, and grid connectivity.

Asset-Light Model

Does not own power assets; focuses on execution capability, reducing balance-sheet risk.

Project Execution Revenue

Earns contract-based revenues through fixed-price or milestone-linked EPC contracts.

Competitors

Tata Power Solar

Strong PSU-backed EPC with execution scale.

Larsen & Toubro (L&T)

Infrastructure major with renewable EPC vertical.

Waaree Energies EPC

Strong domestic solar EPC and manufacturing linkage.

Azure Power

Utility-scale solar developer with EPC capabilities.